Samaaro + Your CRM: Zero Integration Fee for Annual Sign-Ups Until 30 June, 2025

- 00Days

- 00Hrs

- 00Min

1

2

3

→

Bottom Line:

A budget defense is not a recap; prepare answers, not slides about what happened.

The questions are predictable. The answers should be ready.

It is annual planning season, and you have one meeting to keep next year’s event marketing budget. The person deciding is the CFO, not your CMO. They will not ask how the keynote landed or whether the booth looked good. They will ask what the events cost, what they returned, and why the money should not go somewhere else.

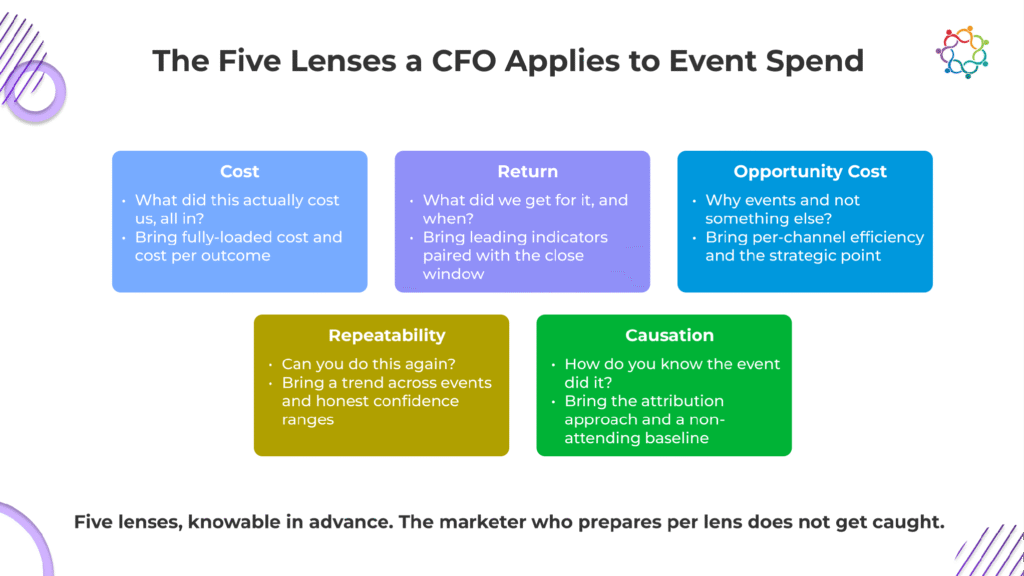

The good news is the questions are predictable. A CFO’s questions about event spend fall into five groups: what the events cost per outcome, what they returned, why events instead of another use of the budget, whether the result repeats, and how you know the event caused it. The bad news is that most marketers walk into this meeting having prepared a recap of what happened, when the CFO wants answers to those five things.

This piece walks through all five groups, the specific data to have ready for each, and the way a CFO reads your answers. The full bank of all 20 questions, grouped and answered, is at the end. Treat the meeting as a known exam. The questions are sitting right here. The only variable is whether you walked in with the answers.

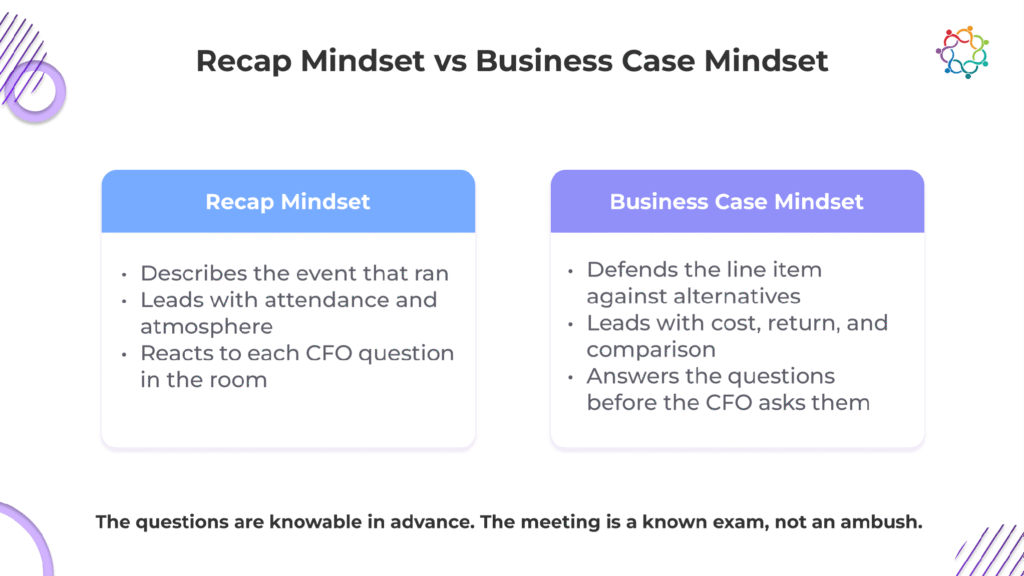

The instinct is to treat this meeting as an ambush to survive, and to hear every question as an attack on events. That instinct is what loses the budget.

Reframe it. The CFO is not attacking events. They are allocating a fixed, often shrinking, pot of capital, and their job is to de-risk every dollar of it. Gartner’s CMO Spend Survey found marketing budgets down to 7.7 percent of company revenue, from 11 percent before the pandemic, with only about a quarter of CMOs saying they have enough to fund their plans. When the pot is that tight, finance has to interrogate every line. That scrutiny is the role doing its job, and it lands on every budget request the same way, events included. That is also exactly why the questions are predictable. The lens is the same in every budget meeting, which is what makes it possible to prepare.

So change what you prepare, because that is what changes how you defend event spend in a budget review. A recap describes the event: attendance, highlights, and how it felt. A budget defense answers what finance will actually ask, and those are two different documents. The marketer who anticipates the questions and walks in with the number reads as a peer who thinks like finance, and that is how a budget gets protected year after year, rather than rescued once.

There is a quieter reason most marketers cannot answer on the spot. The data is scattered across the tools that ran the event, and assembling it takes weeks. The fix is to have the answers already in hand when the meeting starts, instead of reconstructing them under a deadline.

The trap to avoid is bringing the post-event recap deck and expecting it to double as the budget defense. It covers the wrong material and misses the questions that decide the budget.

A CFO almost always opens with cost, and they mean the fully loaded cost rather than the sticker price. The real question is what the event cost in total, and how efficient that was per outcome. Expect questions like “What did this event cost us all in, including team time?” and “What did each qualified opportunity end up costing?”

If you bring one thing to a marketing budget meeting, make it cost in two layers:

A CFO thinks in unit economics, so the per-unit figure is the one that lands. Bringing cost per qualified opportunity, rather than a single large total, shows you already do the math the way they do.

The trap here is quoting only the visible line item, the sponsorship fee, and getting caught when the CFO adds the hidden costs themselves. Travel, the booth team’s week, the content produced for the stand, all of it belongs in the number. Bring the fully loaded figure first, before anyone has to ask for it. It signals that you are not rounding down to make events look cheaper than they were.

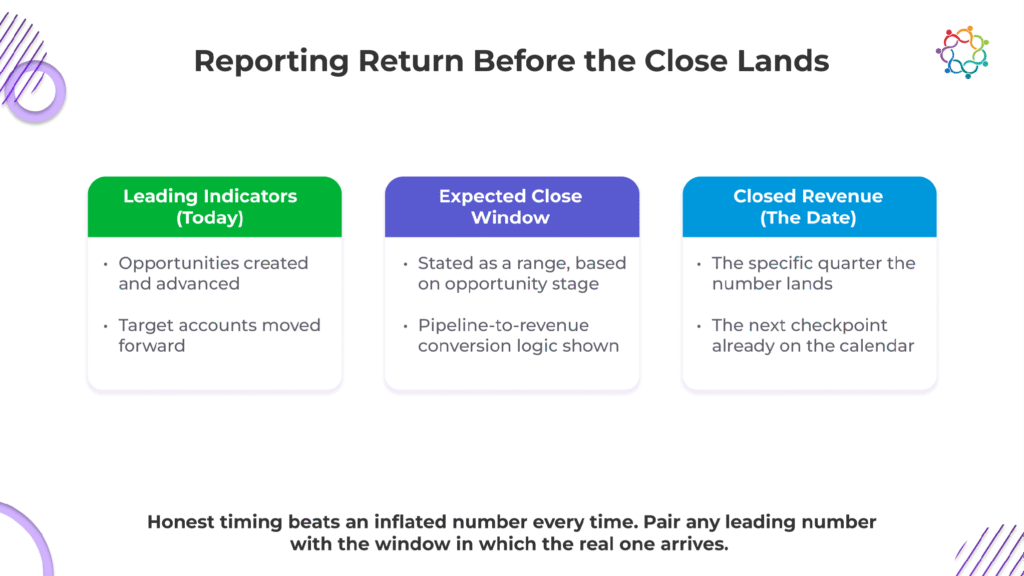

Cost handled, the CFO turns to the return, what came back, in the pipeline and in closed revenue and when. Expect “How much pipeline did this create?” and the sharper follow-up, “How much of it has actually closed?”

Have ready the opportunities the event created and advanced, with values attached. The honest complication is timing. This is really the question of how to present event ROI to finance when the close is still months out. In most B2B cycles, the deals an event influences close well after the event, often after the budget meeting itself. When nothing has closed yet, do not paper over it. Bring the leading indicators, meetings booked, opportunities created, deals that moved a stage, and pair each with the window in which the closed number is expected to land. Honest timing beats an inflated figure, because a CFO has seen inflated figures before.

This is exactly what a pre-close event recap is built for, reporting an event’s return before the revenue arrives. That recap is the artifact that already holds these answers, so the budget meeting becomes a matter of opening it instead of rebuilding it.

The trap is leading with a big “influenced pipeline” number that has no closed revenue behind it and no date attached. To finance, an influential number with no timeline reads as marketing math, the kind of figure that invites more scrutiny instead of less. Any leading number you bring should travel with the date the real one arrives.

This is the opportunity-cost question, and it is where many marketers get stranded. The CFO is splitting a fixed budget, so the real question is why this money belongs in events instead of paid, content, or another hire. Expect “How does event ROI compare to our paid channels?” and “What would we lose if we moved this budget to demand gen?”

The core of how to justify an event marketing budget to a CFO has two parts. First, a like-for-like efficiency comparison: your event cost per opportunity set directly next to the cost per opportunity from your other channels. Second, the strategic point a spreadsheet misses is what events do that no other channel can:

To a CFO dividing a fixed pot, “events are valuable” loses to “events are more efficient than channel X for this segment, and they do something no channel can.” Bring the comparison and the distinction together. One without the other is half an answer.

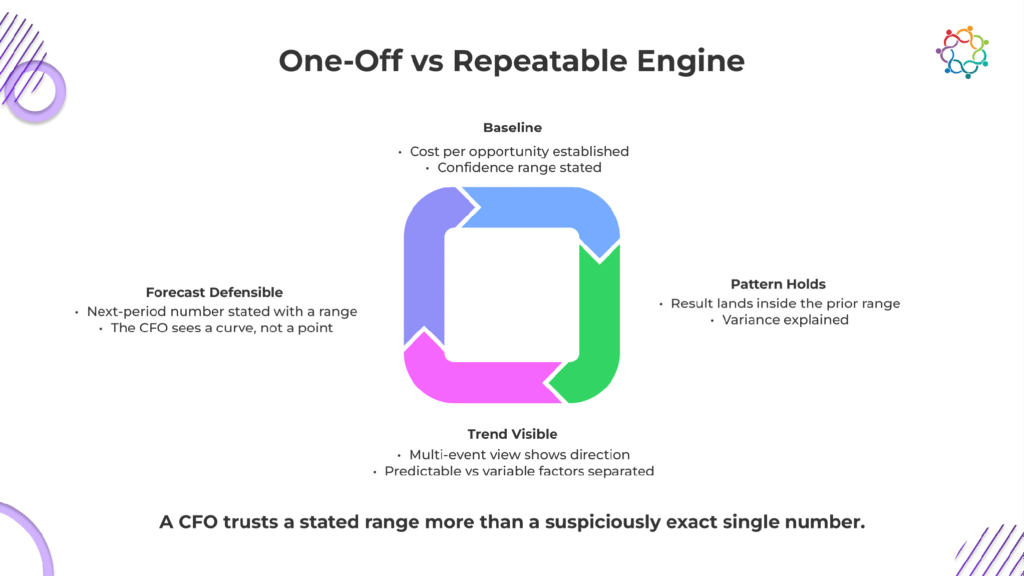

A budget is a forecast, so the CFO needs to know the return repeats. The real questions are whether this was a repeatable engine or a lucky one-off, whether you can predict next period, and how far to trust your figures. Expect “Was this a one-off, or can you predict next quarter’s return?” and “How confident are you in these numbers?”

Three things answer this. Show a trend across several past events, so the result reads as a pattern rather than a single lucky point. Separate clearly what is predictable from what is variable, the reliable floor against the upside that depends on the specific event. And give honest confidence ranges in place of suspiciously exact figures. A CFO trusts a stated range, “we would commit to this floor, with upside to here,” more than a single number carried to two decimal places.

This is the heart of defending an event marketing budget to leadership over time. A budget survives on a credible forecast of the next several quarters, more than on a single strong one.

The trap is taking one excellent event and projecting it forward as the baseline or presenting estimates as though they were measured facts. Over-confidence costs you a CFO’s trust faster than a candid “here is the range we are willing to stand behind.” Once a number looks too good, every number you bring after it gets discounted.

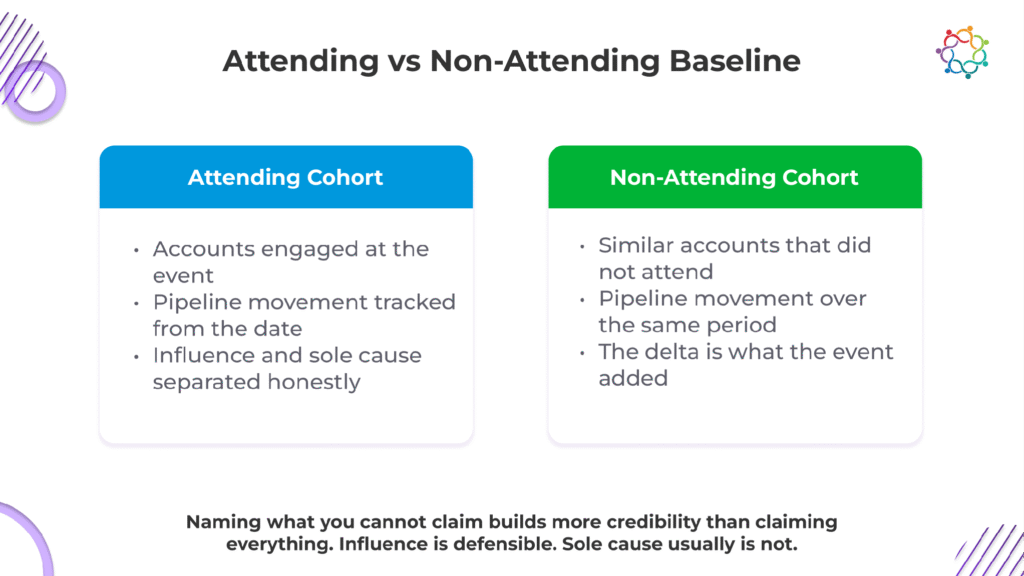

This is the skeptical question, and the one where overclaiming does the most damage. The CFO wants to know causation: were these deals you would have won anyway, and how exactly are you crediting them to the event? Expect “Aren’t these accounts we’d have closed regardless?” and “How are you attributing this pipeline to the event specifically?”

Here is how to answer the hardest CFO questions about events. Bring three things, and keep them plain:

Naming what you cannot claim builds more credibility than claiming everything, because it tells the CFO you are reading the data straight. The same attribution discipline runs through our Event Sponsorship Measurement Framework.

The trap is claiming the event was the sole cause of every deal it touched. Overclaiming hands the CFO a clean reason to discount the whole number: if one claim is obviously inflated, why trust the rest? Claim the influence you can defend, concede what you cannot, and the number you are left with carries more weight than a bigger one nobody believes.

The questions are not a mystery. They fall into five predictable groups: cost, return, comparison, repeatability, and causation, so the work is to prepare the data for each group before you walk in.

The marketer who keeps the budget is not the one with the best event. It is the one who walked into the room already holding the answer to every question the CFO was going to ask.

All 20 questions, grouped the way a CFO thinks, each with the data to have ready and a sample answer you can adapt, are in the full CFO Event Budget Question Bank, along with a one-page prep checklist for your next budget meeting. It takes your first name, work email, company size, and role.

To see how running events in one place keeps these answers ready instead of scattered across tools, book a walkthrough.